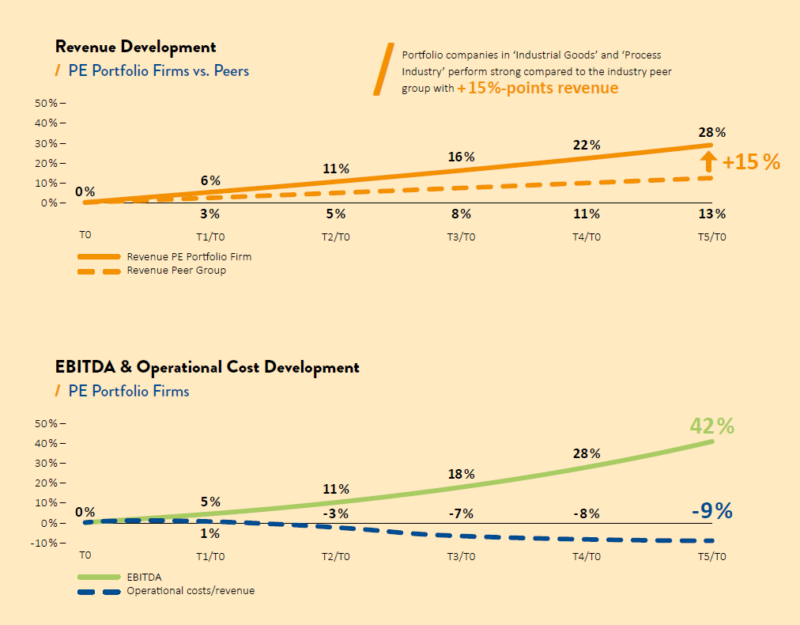

Portfolio companies experienced a significant increase in value in the first five years after being acquired.

Looking at the industrial goods and process industries, our long-term analysis indicates that mistrust in private equity firms is largely unfounded. As our figures show, many private equity firms tend to take a long-term approach and are focused on sustainable business success.

The challenges of the coronavirus pandemic have hit companies hard, so they are on the lookout for investors. At the same time, private equity firms have significant amounts of capital at their disposal (referred to as dry powder), creating promising opportunities for both sides.