Private Equity White Paper 2021

Private equity companies have recently pulled out all the stops in the top and bottom lines to defy the pandemic and stabilize margins. A closer look, however, reveals that not all potential for operational value creation has been exhausted. Procurement in particular still has a lot to offer in terms of cost optimization.

Private equity companies and their portfolio companies have so far come through the pandemic mostly unscathed. This is shown by a private equity study conducted by INVERTO in the first quarter of 2021. Although the vast majority of PE companies have recorded declines in turnover in their portfolio companies, these have only had an impact in the form of falling profits for a good half of the participants.

Compared to the situation before the pandemic, private equities initially acted much more defensively. The focus on expansion and add-on acquisitions has lost relevance compared to 2019. This is surprising, as the majority of respondents see increasing, or at least unchanged, investment opportunities in a largely price-stable investment market. This temporary defensive situation, as well as the existing ‘dry powder‘, is now driving the willingness to invest, which has been on the rise again since the third quarter of 2020.

Private equity companies are currently focusing more on the bottom line of their portfolio companies. Due to the pandemic, value enhancement measures with an early direct impact are in the foreground – for example, negotiation programs. These levers are necessary and effective. They can be used to achieve results quickly. However, their effectiveness is limited.

Find out in the following, based on the results of the study, which approaches to optimization should now come into focus and which aspects need to be considered in order to generate sustainable cost advantages.

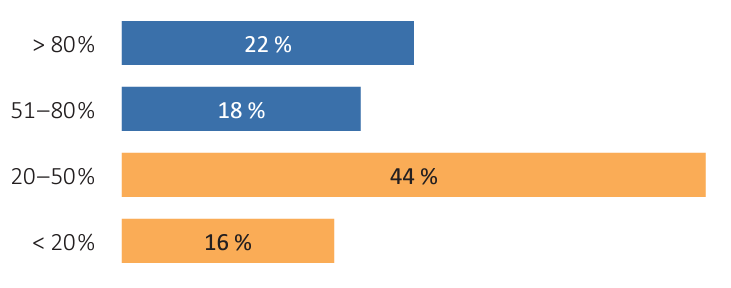

Share of companies financially impacted

“How many of your portfolio companies have been financially impacted negatively through Covid-19?”

The majority of PE firms surveyed indicate that 50 percent or less of their portfolio companies have been negatively impacted financially by the Corona pandemic. This indicates diversified and strong portfolios on the part of the participating private equities.

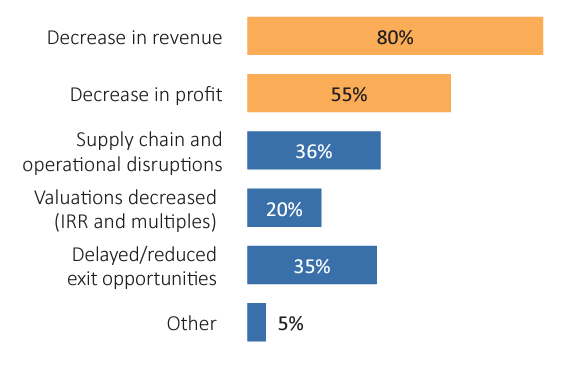

Negative impact through Covid-19

“In which ways have your portfolio companies been negatively impacted by Covid-19?”

Looking at the effects of Covid-19 in detail, more companies complain about turnover losses than profit declines (80 versus 55 percent). The respondents therefore seem to have partly succeeded in stabilizing profits through countermeasures – despite a decline in turnover.

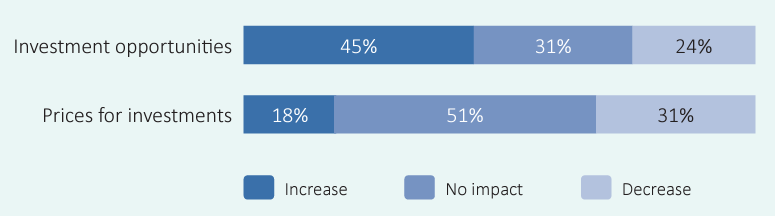

Rising investment opportunities with stable prices

”What impact does Covid-19 have on your deal flow?”

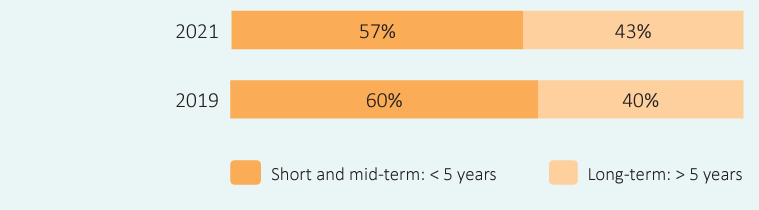

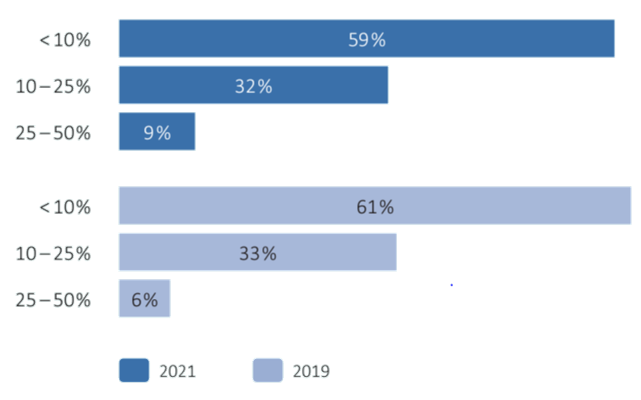

Holding period of investment activities

45 percent of the PE companies surveyed see increasing investment opportunities for their deal flow through Covid-19. This development – as confirmed by a good half of the participants – contrasts with stable prices for investments.

The holding period of portfolio investments remains largely unaffected by the pandemic and is stable compared to 2019. Around two-thirds of PE companies continue to hold their portfolio for up to five years, 43 percent beyond that.

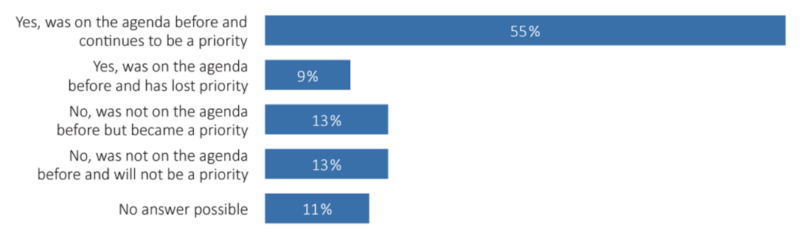

ESG prioritization remains unchanged

Also unaffected by the crisis is the prioritization of one of the most important strategic issues for the future: Environmental, Social and Governance. ESG have not lost their relevance for medium- and longterm strategy development and continue to be a priority for the majority. This is also in line with the demands of society to attach greater importance to the topic of sustainability.

“Has ESG been on your portfolio’s agenda before the Covid-19 crisis? Have the priorities changed?”

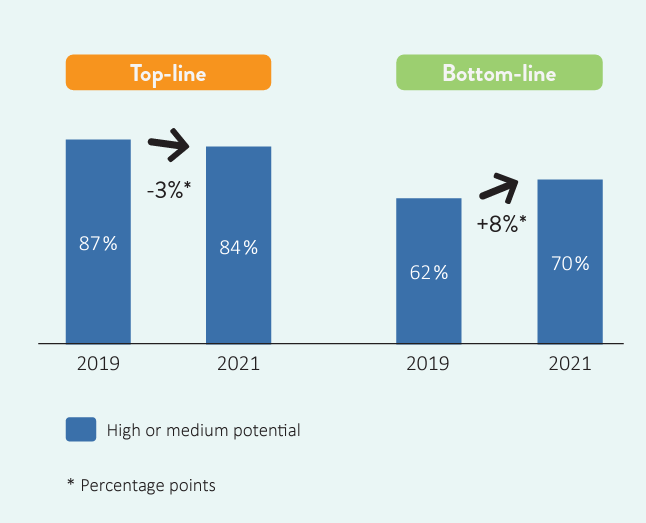

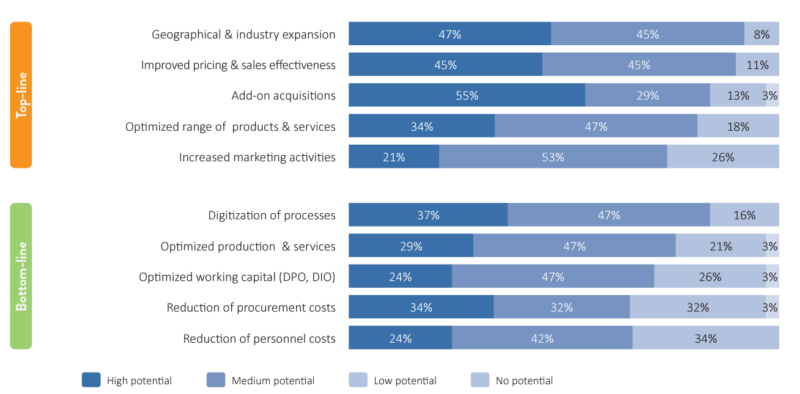

Momentum for top-line and bottom-line measures

Covid-19 is having a significant impact on the value enhancement approaches taken by private equities. Especially bottom-line measures are gaining significantly in importance. Obviously, PE companies perceive that in the current situation they have to pull out all the stops to secure their earnings targets. In particular, repeated (threatening) corona-related closures have necessitated rapid action.

Top- vs. bottom-line development before and during the crisis

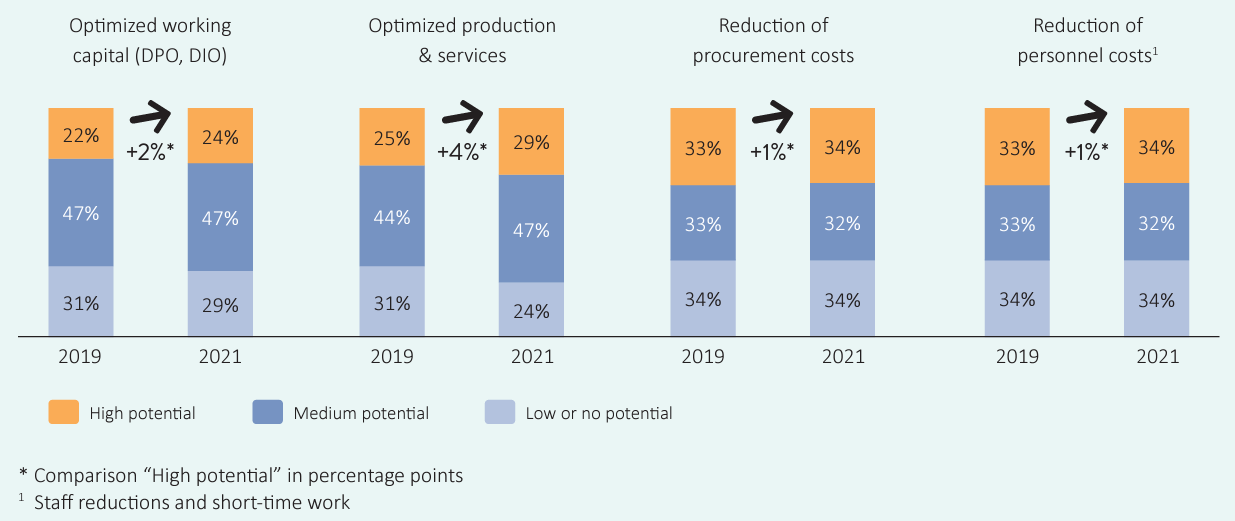

In the bottom-line, high potential for value creation is currently attributed in particular to the digitization of processes (37 percent) and the reduction of procurement costs (34 percent).

Comparing the estimated potential of the various bottom-line approaches with the 2019 study, it is noticeable that the topic of personnel cost reduction has increasingly moved onto the agenda. This is understandable as, unlike in classic economic crises, many companies were obliged to restrict their business activities, or even close down due to the pandemic. We assume that in many cases this is more a case of short-time work than redundancies.

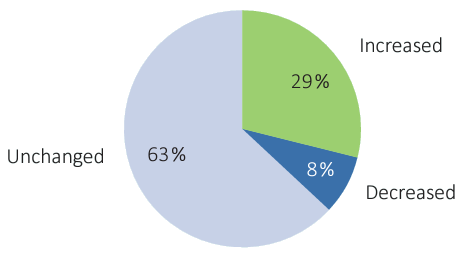

Operational value creation: The role of procurement in the crisis

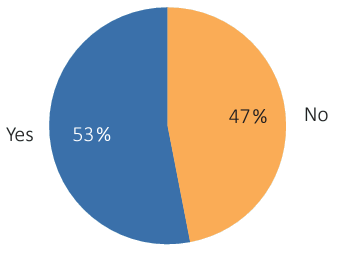

Procurement continues to gain importance as a value-enhancing lever. Nevertheless, only just over half of the companies set procurement targets to exploit their value creation potential. While the trend is upward – even before the pandemic, about 42 percent of the PE firms surveyed said they set procurement targets for their portfolio companies – the lack of targets still represents a deficit that needs to be addressed.

-

“Has the importance of procurement as a value creation lever changed?”

-

“Are you setting goals for your portfolio companies with regard to value increases through procurement optimization?”

-

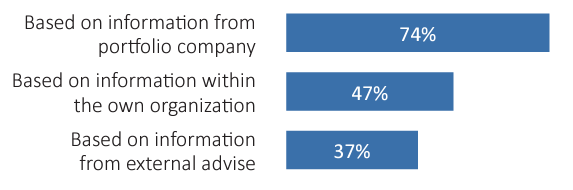

Taking a closer look at the process of target definition, it becomes clear that the majority of PE companies base their decisions only on internal information. This information comes from the portfolio companies or originates in their own organization.

-

“How do you define goals for procurement?”

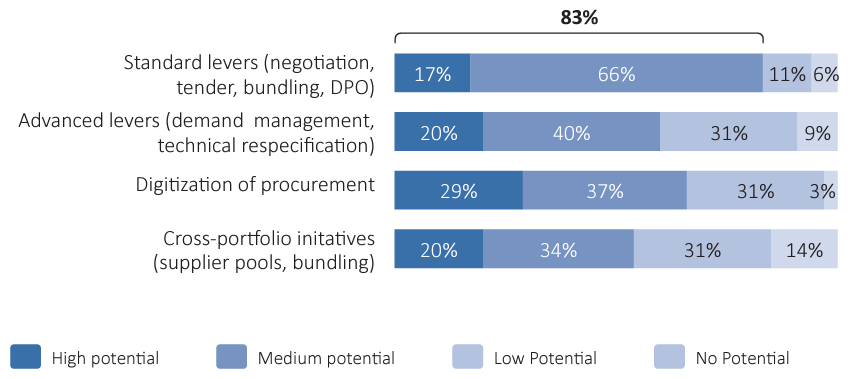

Increase in importance of procurement levers with early & sustainable impact

![]()

While standard procurement levers such as negotiation, tendering, bundling or Days Payable Outstanding (DPO) show a similar level of application compared to the 2019 study, they continue to gain importance as early-impact levers in the pandemic. At 83 percent, they appear most promising to participants for improving the bottom line.

In principle, 29 percent of the participants attribute the highest potential to the digitization of procurement. At the same time, half of the PE companies surveyed state that this lever is not yet being fully exploited. A similar picture emerges in the context of consulting projects. However, the use of spend analytics and e-procurement tools such as “e-auctions” is now gaining momentum.

Importance of procurement cost optimization

Assessment of procurement measures in terms of their potential to improve the bottom line of a portfolio company

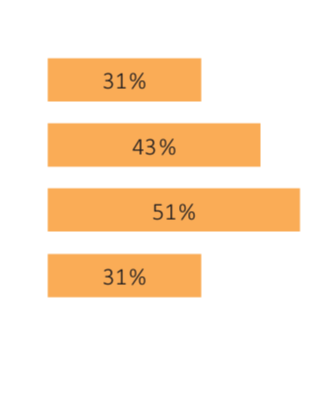

Not fully utilized levers for value creation

“Which group of procurement levers do you consider as not fully utilized to create value during your previous investment activities?”

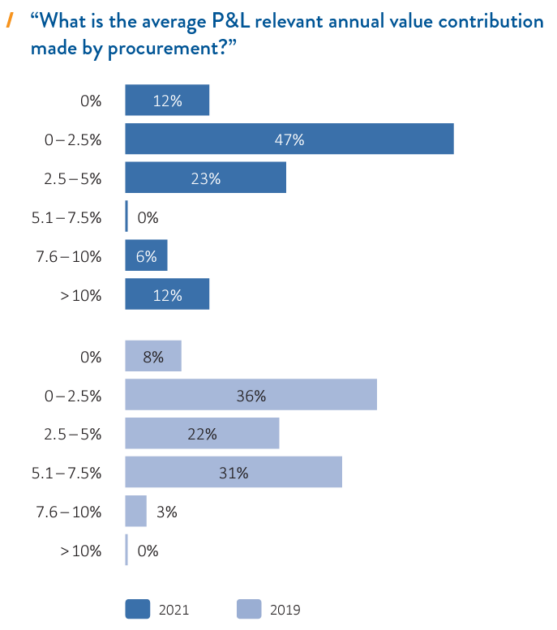

Significant differences in the value contribution of procurement

Comparing the P&L-relevant annual value contribution of procurement (2019 vs. 2021), it is noticeable that the share of companies whose procurement value contribution ranks in the “midfield” (5.1–7.5 percent) is dwindling.

Value contribution of procurement during exits

Differences in the contribution of procurement to value creation are also clearly evident in exits after an average of five to six years. While the majority indicate an overall contribution by procurement of up to ten percent, the most successful buyers achieve value contributions of over 25 percent.

Compared to 2019, the share of exit cases with a value creation contribution by procurement > 25 percent has grown by three percentage points.

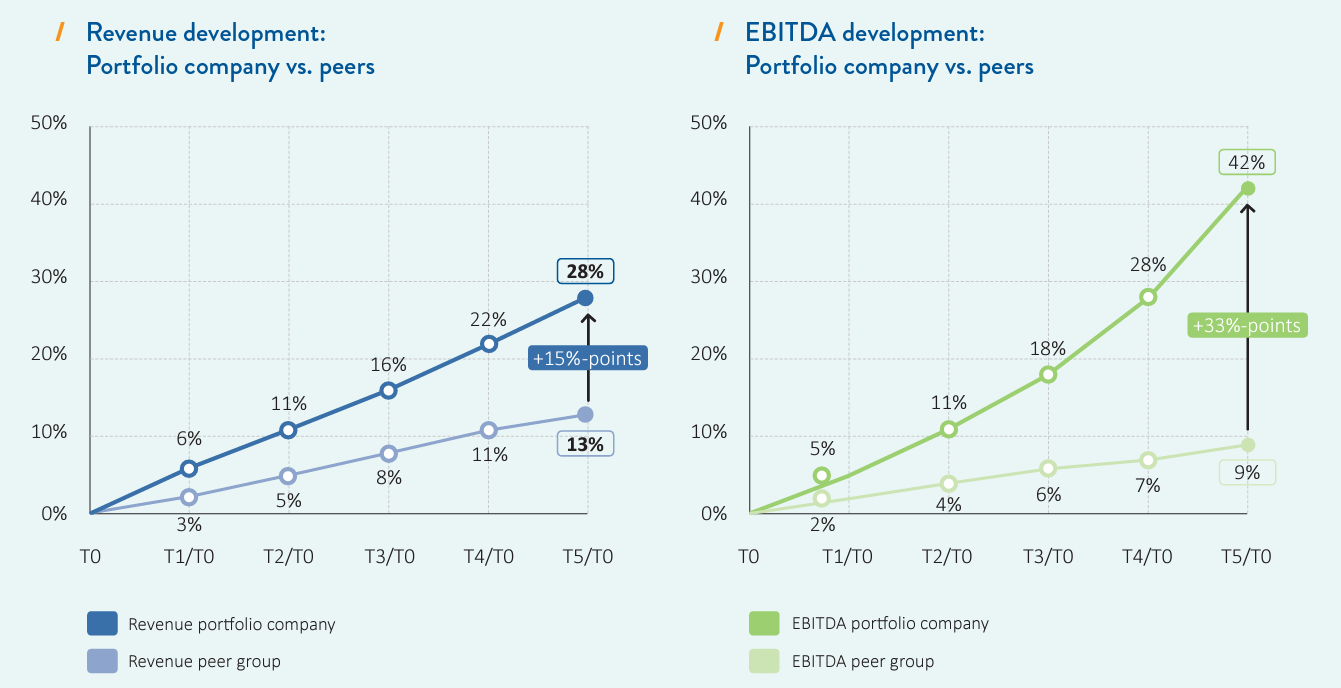

Excursus: Top performers before the pandemic

In a quantitative analysis, INVERTO compared the performance of portfolio companies from the industrial goods sector and the process industry with companies without PE involvement (peer group) from 2013 to 2018*.

The most important finding of the study: Private equity companies achieved a significant increase in the value of their portfolio companies. They achieved significantly higher EBITDA and revenue growth than companies without PE involvement. This observation holds true over the entire five years, with the gap widening from year to year.

Portfolio companies record an average growth in revenue of 28 percent during the period under review, while companies without PE involvement achieve 13 percent. The difference in EBITDA is even more significant: here, portfolio companies achieved an increase of 42 percent, while the comparison group had to settle for nine percent.

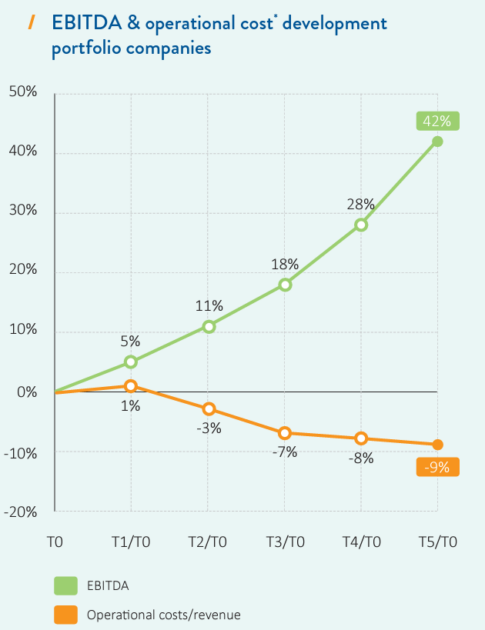

The analysis further shows that, in relation to revenue, the other operating expenses of portfolio companies tend to decrease within two years of acquisition by the private equity company and even fall by an average of nine percent over the five-year period under consideration. This improvement in other operating expenses, in addition to the pure revenue-based growth, contributes significantly to an increase in EBITDA.

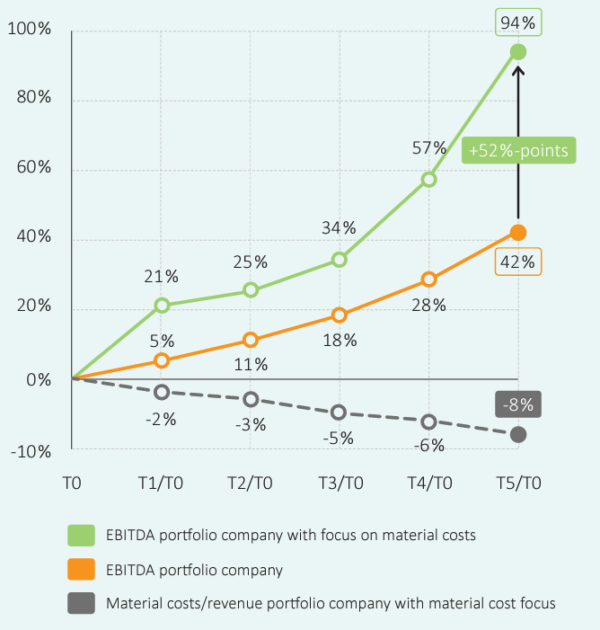

“Best-in-class“ EBITDA growth is only achievable with a comprehensive and sustainable improvement in material costs. The top class among the portfolio companies convinced with a strong focus on material cost reduction and thereby increased its EBITDA growth to 94 percent over the five-year period under consideration.

Operational excellence: How the wheat is separated from the chaff in procurement

In uncertain times, the entire portfolio of short- and long-term measures within the bottom line becomes more relevant. An expansion of operational value creation is therefore inevitable. In order to be able to take all measures effectively and exploit them to the full, additional resources, which must be considered early in the planning process, are indispensable. This includes, on the one hand, increasing the number of experts, or organizing experts, in order to generate high value contributions even in the short term. On the other hand, a strategic investment in digital tools and forward-looking topics such as ESG should not be neglected. Basically, it is always important to set clear and ambitious optimization goals.

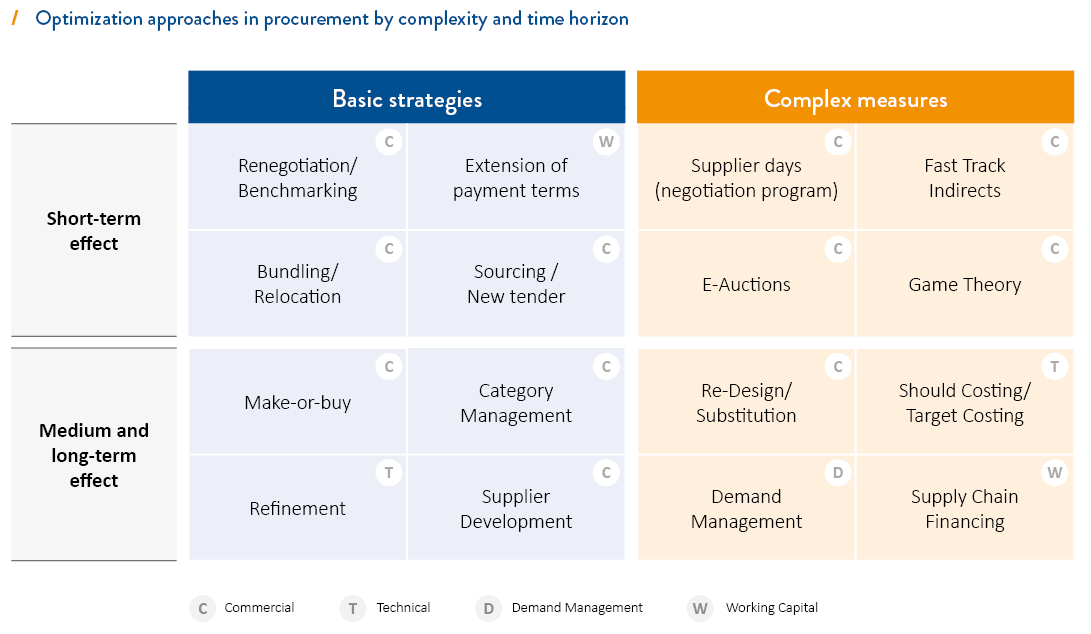

1 Short-term focus with foresight on complex, sustainable measures

Fast-acting basic strategies such as negotiations, tendering, bundling or DPO optimization help to compensate for possible sales slumps and support stable profit development in an uncertain market.

These measures are necessary and lead to quick results. However, their effectiveness is limited. To realize the full potential for cost reductions, companies should also work with more complex measures such as demand management – the precise analysis of all needs – or technical re-specification – for example, the search for substitutes for expensive raw materials. Private equity companies are well aware that they could do more in this area: 43 percent of the study participants see untapped potential in the area of sophisticated levers.

Optimization approaches in procurement by complexity and time horizon

Complex measures with short-term effect

![]()

Taking into account the increased relevance of quick and direct cost reductions, complex measures of a commercial nature offer considerable potential.

Instead of classic renegotiations, for example, a large number of suppliers can be approached via a dedicated event-driven negotiation program. Within the framework of a so-called Supplier Day, A and B suppliers are invited by top management to a (virtual) event. In block or individual negotiations that immediately follow, savings and optimizations are fixed with decision-makers.

Experience has also shown that the institutionalization of renegotiations in accordance with fixed threshold values releases considerable potential. For example, all expenditures in the area of Indirect Spend and CapEx can be analyzed by a so-called Fast Track Team, compared with benchmarks, and renegotiated depending on the approval decision.

Successes achieved through the use of digital negotiation tools do not necessarily have to wait until the complete digitalization of procurement is complete. For example, deadlocked sourcing scenarios can be resolved via so-called e-auctions, a form of auction via electronic portals.

Sustainable savings through timely focus on technical levers

In order to optimize costs sustainably, it is important to take measures with a medium- and long-term time horizon at an early stage. Technical levers are particularly suitable for this purpose; although they involve a longer lead time, they offer great potential.

One effective measure is the fundamental review of demand specifications with subsequent refinement. In this process, specifications are minimized and rolled out as a new standard, often across locations. This technique is used, for example, when a company has different packaging units for fundamentally similar products in use at various locations. Refinement can be applied to technical requirements of the direct procurement volume as well as to indirect requirements and services.

In addition, a re-design of the requirements is also possible. In a re-design, the fundamental nature of a product, for example packaging, is questioned. The analysis includes the concept (what do I need to protect in the first place), the construction (geometry and structure) as well as the material used (corrugated board vs. plastic or metal). The introduction of completely new concepts is often associated with sudden cost reductions.

Data-driven approaches such as Should Costing have also become much simpler and more common. Today, it is possible to carry out Should Costing analyses on the basis of a broad database and thus to identify potentials with the respective suppliers, but also in the internal value creation, in comparison to the existing costs. These optimization possibilities can be implemented in the short term within the framework of negotiations or in the medium term in the course of supplier developments.

The amount of savings that can be achieved with technical levers is highly dependent on the initial situation and the purchased components and, according to experience from INVERTO projects, averages around 14 percent.

Working capital and supply chain finance as a means of crisis management

However, optimizing working capital must not be a temporary agenda item. Continuous

The degree of success of working capital measures depends on the management model that is aligned with the corporate strategy. In addition to clearly defined working capital responsibilities, especially at the operational level, the model must include analyses, targets, KPIs and a working capital reporting system. Only then can capital efficiency potentials and capabilities within the organization be fully leveraged and released.

When companies and their suppliers simultaneously try to optimize their working capital for high cash balances, problems can arise. Reverse factoring or supply chain finance provide the appropriate solution in such cases. With these financial instruments, working capital and liquidity are managed more effectively. Supply chain finance involves the various actors along the supply chain and does not rely on classic loans. Ultimately, the aim is to create high levels of cash and low levels of inventory. Invested wisely, the money can work for companies and thus generates returns despite the low-interest phase. Cooperating with financial partners to free up capital through individually agreed payment terms opens up additional opportunities for private equities and can help achieve KPIs associated with working capital.

2 Setting ambitious and realistic procurement targets

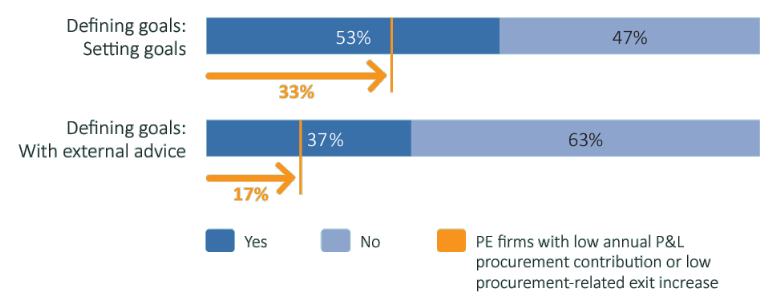

Procurement performance is strongly linked to the setting of targets. With consistently high asset multiples, realistic but also ambitious targets must be defined. It is therefore still surprising that only just over half of the respondents (53 percent, see chart page 8) set targets for their portfolio companies regarding value enhancement through procurement optimization.

Value contribution by procurement

Differences between all participants and PE firms with either annual P&L procurement contribution <2.5% and/or procurement-related exit value increase <10%

As the results of the INVERTO survey suggest, weak value creation contribution of procurement can be attributed to deficits in the definition of procurement targets. PE companies with low annual P&L procurement contribution and/or low procurement-related exit value creation hardly ever set targets (only 33 per cent) and rarely use external consultants in target definition (only 17 percent).

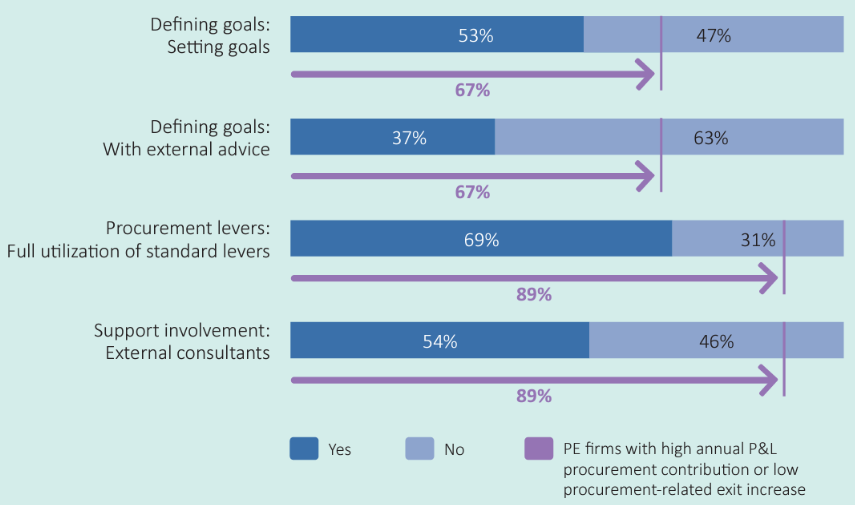

Profile of top procurement performers

However, the consistent inclusion of industry and procurement expertise in strategy formulation is crucial. PE companies with higher annual P&L procurement contribution and/or high procurement-related exit value mostly increase set targets (67 percent) and use external consultants (67 percent). The majority also use the complete standard procurement optimization set (89 percent).

Differences between all participants and PE firms with either annual P&L procurement contribution >7.5% and/or procurement-related exit value increase >10%

External support for fast results and high value generation

Experience shows that the buyers of the portfolio companies hardly manage to achieve significant additional savings without support in addition to the tasks of day-to-day business. Ideally, therefore, they receive support from procurement experts from the private equity company itself or from external consultancies.

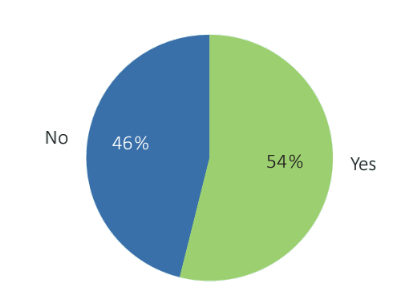

This observation is confirmed by the study. Just over half (54 percent) of the private equities surveyed use external consultants in the operational areas of their portfolio companies.

Involvement of external consultants

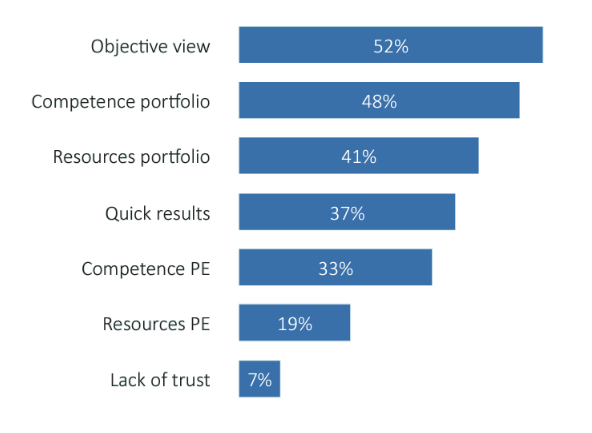

The main reasons for hiring a consulting firm are the need for an objective view (52 percent), a lack of professional expertise within the portfolio company (48 percent) and a lack of human resources.

Especially when there is a need for quick action, calling in external support is therefore crucial to success. The figures speak for themselves: 89 percent of the top performers resort to external support to increase their value creation.

“Do you involve external consultants to increase value for the portfolio companies?”

“Why do you employ external consultants?”

3 Strategic investments in digitization and sustainability of procurement

It is also important to stay on the ball when it comes to sustainability. According to the survey, the so-called ESG criteria (Environmental, Social and Governance) have indeed not lost their importance. 55 percent of the PE companies surveyed confirm that sustainability criteria play

A good half (51 per cent) of the respondents have recognized that the digitization of procurement must continue to gain in importance. However, there is also agreement that the advantages and opportunities opened up by digitization are still largely untapped. The problem is mainly due to the selection and investment required to implement digital solutions. If done intelligently, however, digital projects quickly produce a measurable return on investment. In order to secure a significant competitive advantage in the long term, PE companies should definitely push the issue.

In order to create social and ecological added value, ESG must be further addressed and pursued. As an interface and ESG „implementing body“, the goals and activities of procurement must therefore be defined and aligned with the ESG agenda.

We are seeing a increase in sustainability interest and ESG solutions in procurement. Especially in the PE environment, this goes beyond pure sustainability ratings. Holistic concepts that include the entire procurement organization are in demand here.“

Markus Bergauer, Managing Director and sustainability expert

Conclusion

The success of procurement – and thus of the entire company – is based to a large extent on ambitiously set targets and the consistent application of professional methods. In order to master current and future challenges, resources for optimizing operational value creation must be expanded at an early stage. PE companies achieve a quick, direct and higher impact by resorting to experts from their own PE organization or externally. As well as the additional resources needed to exploit the full optimization set, they can provide an objective assessment and compensate for missing competencies in the portfolio companies.

Fast-acting procurement levers do help to compensate for possible sales slumps and support stable profit development in an uncertain market. However, for sustained success, they must in any case be complemented by complex and long-term measures. Strategic investments in digitziation sustainably improve procurement performance and should definitely be pursued. As sustainability criteria become increasingly important for companies, PE companies need to ensure that the objectives of procurement in their portfolio companies are aligned with the defined ESG criteria. In this way, procurement can optimally contribute to creating social and environmental added value.

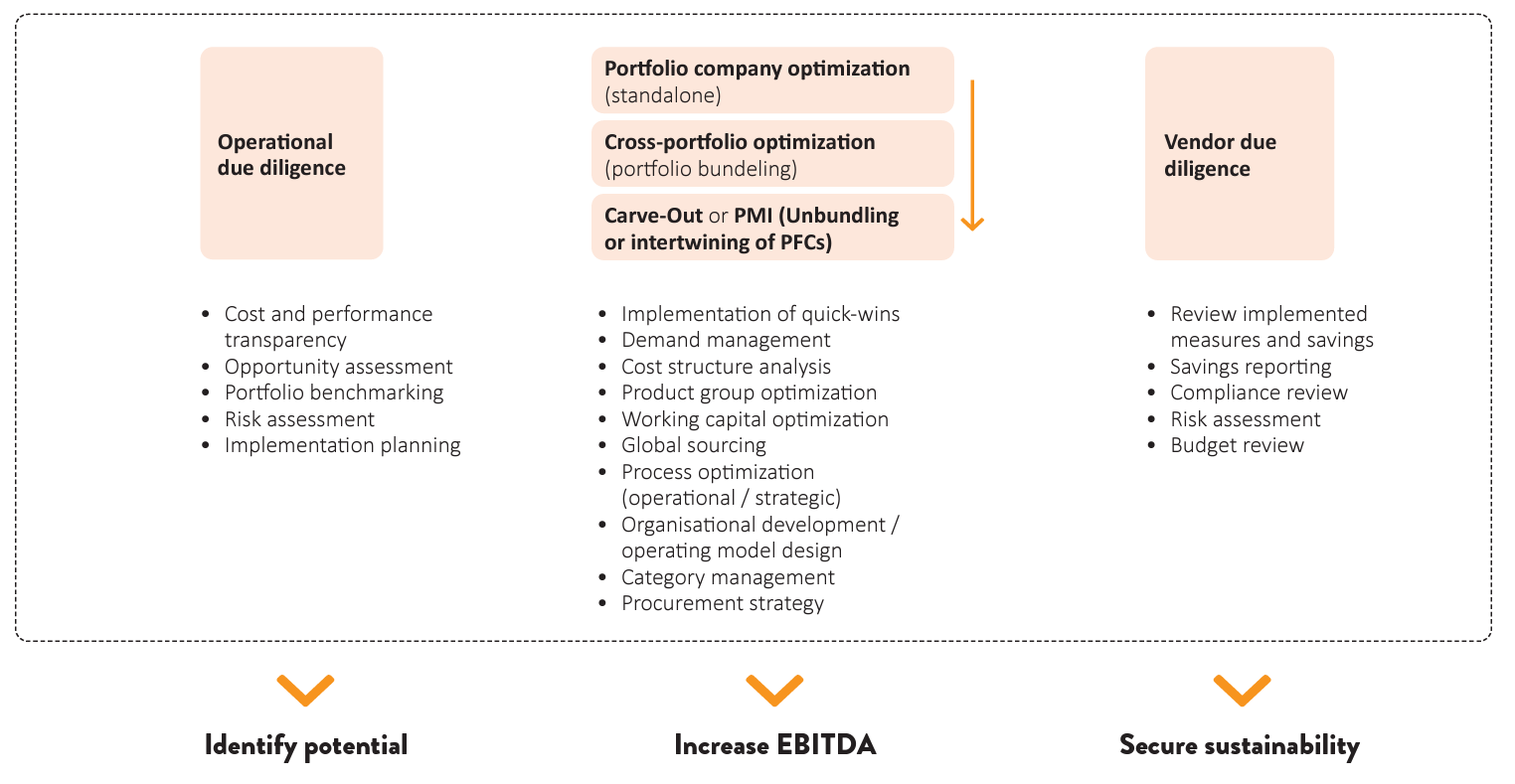

INVERTO Private Equity Services

Our support in procurement along the entire private equity investment process

![]()

Private Equity White Paper Download

Best-in-class portfolio companies: Exploit value creation potentials in and after the pandemic

Study results, opportunities and recommendations for action by INVERTO