In a long-term move towards environmental sustainability, the European Union (EU) has unveiled the Carbon Border Adjustment Mechanism (CBAM). This regulation, a main pillar of the EU’s ambitious green deal, aims to combat climate change by significantly reducing greenhouse gas emissions. From 2026, CBAM will introduce new tariffs on imported products from outside the EU based on their contained carbon.

Importers will be required to acquire certificates corresponding to the total emissions of imported goods, priced at the prevailing rate of CO2 in the EU. This measure targets the following carbon-intensive goods: aluminium, cement, electricity, fertilizers, hydrogen and steel. Incorporating Scope 1 emissions from production facilities and Scope 2 emissions from electricity usage during manufacturing, CBAM is taking a comprehensive approach to carbon accounting. However, it’s important to highlight that CBAM does not cover emissions falling under Scope 3 categories, such as those originating from primary products and transportation.

2024 Raw Materials White paper

Future Proven Raw Material Management

Discover how leading companies are adapting their sourcing strategies to build resilience and stay competitive. Download the white paper to gain valuable insights and prepare for the future of raw material management.

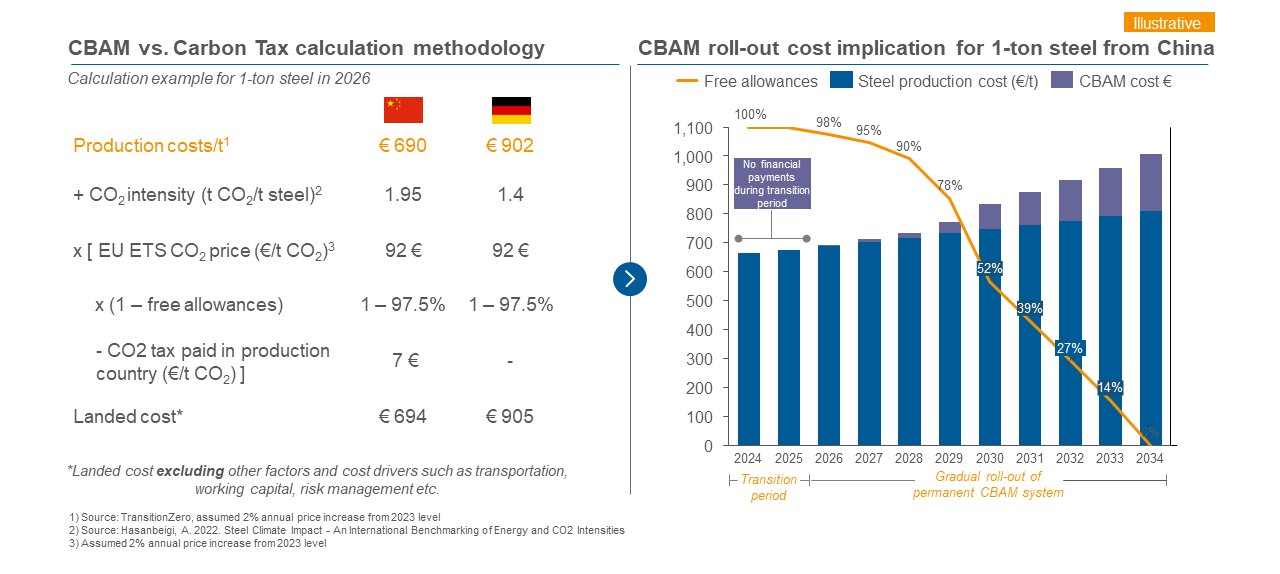

The impact of CBAM regulation across key intervention areas

The resulting increase in cost levels, affecting both domestically produced and imported goods, is set to redefine suppliers’ competitive landscape. Their ability to remain competitive will hinge on the variance in their emission levels.

Beyond cost increases, CBAM will have further implications

-

Supplier engagement & reporting (from 2024 onwards)

Importers must request data on the contained emissions from non-EU suppliers for quarterly reporting.

-

Administration (from 2026 onwards)

Importers must register with national authorities to purchase CBAM certificates and surrender them annually according to contained emissions.

-

Progressive payments (from 2026 onwards)

Importers will have to pay for the CBAM in stages, to the extent that European suppliers start paying for their emissions.

Which specific measures should companies take in order to comply with CBAM?

- Create transparency of goods imported from non-EU countries on a supplier level within the scope of the regulation

- Prepare quarterly reporting of emissions contained in imports. Apply EU default values during the transition period for goods for which no specific supplier emissions are available

- Conduct a preliminary financial impact assessment of the gradual roll-out of CBAM from 2026 to 2034 taking into account emissions included in imports, free allowances and CBAM costs

- Engage with your non-EU suppliers to collect product and supplier-specific emissions data now, which has to be included in quarterly reporting from 2026 and onwards

- Refine the impact assessment and develop a strategy based on financial impact and a sustainability roadmap as more supplier specific data is collected

Get in contact with our experts

Authors

Lars-Peter Häfele

Managing Director

is Managing Director at the Munich office and an expert in raw materials. He advises major global companies in the industrial goods and automotive industries.

Patrick Lepperhoff

Managing Director

is a Managing Director at Inverto in Cologne. As head of the Supply Chain Management Competence Center, he mainly supports customers from industry and consumer goods production.

Our expertise related to CBAM