EU strategy: Reduce dependence on raw material-producing countries

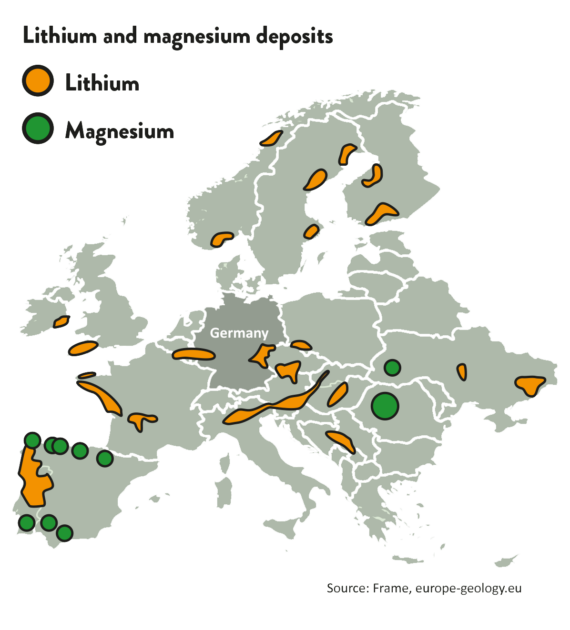

An intensified use use of recycled materials would also reduce Europe’s dependence on the countries where the raw materials are stored or refined. Currently, the EU produces only three % of the raw materials it consumes. China has built up a central position of power: For rare earth, for example, almost 100 % of imports come from China, and for magnesium, the figure is just under 90 %. Around two-thirds of cobalt come from Congo, despite criticism of the human rights protections in the Central African country. Lithium is mainly supplied from Latin America – but because of the environmental damage, more and more inhabitants are fighting against existing and planned plants.

For rare earth, cobalt and lithium, recycling is not yet a real option. For cobalt, the raw material required for batteries, more and more customers – such as car manufacturers – are choosing individual solutions by concluding contracts directly with mine operators operating in ESG-compliant countries such as Australia or Canada. Lithium, on the other hand, is not actually a rare commodity. Currently, there are pilot and research projects in many European countries to develop the deposits. However, local protests have been staged in each of these countries – from Portugal to Finland to Serbia.

Politicians and operating companies therefore still need to build up trust before the first lithium is extracted from European soil. The advantages are obvious: in Europe, it is easier to monitor whether companies are complying with labor and environmental protection laws, additional requirements could further curb environmental risks and, last but not least, transport routes are significantly shorter. Europe could thus create models for sustainable mining. The expertise is there, after all, the continent boasts a centuries-old mining tradition, and environmental protection has also long played a role in the EU. However, it is doubtful that there will be any short-term success here: When even a wind turbine quickly becomes a political issue, companies need transparency, good arguments and staying power to implement projects.